The Value of a Job – Coal and Energy Employment Trends

By Max Dorman and Philip Jordan, BW Research Partnership

The coal sector has been deeply impacted by the low cost of natural gas, the increase in shale exploration and increased attention to zero carbon energy, resulting in a decrease in demand for U.S. coal. Lower demand for U.S. coal has concerning implications for the many workers who make up the coal industry, from workers in mines to wholesale traders. The coal industry lost 17,000 jobs from 2015 – 2019, roughly 6 percent of its total employment. The closure of coal mines, coal generation plants and other businesses poses threats, not only to those employed in the coal industry, but also to the many families and communities that rely on coal wages to support their livelihoods. These communities span the country, from the Appalachian Region in the east to the Illinois Basin in the Midwest to the Mountain West states from Montana and Wyoming south to the Four Corners area. There is no “one size fits all” solution that would address the varying needs of coal-dependent communities; any solution must account for the diversity of industries and skillsets within the coal sector, recognizing that local needs cannot be met with broad-brush promises of a “just transition.” Any solution to our climate problem must be based in the realities of the energy sector broadly and coal communities in particular.

Earlier in 2021, BW Research Partnership, the Energy Futures Initiative and the National Association of State Energy Officials published findings on energy industry earnings in a report which supplements the annual U.S. Energy & Employment Report. Energy sector wages are dependent on experience level, skills, education and other factors such as geographic location, market competition, union representation and the risk associated with the job. The energy source’s industry mix also affects average wages; for example, workers at utilities generally receive some of the highest hourly rates, while energy traders are typically paid significantly less. Another important factor is demand for other energy sources; with the natural gas boom came 73,000 new jobs, which put downward pressure on coal demand and contributed to the loss of 17,000 coal jobs over the same period.

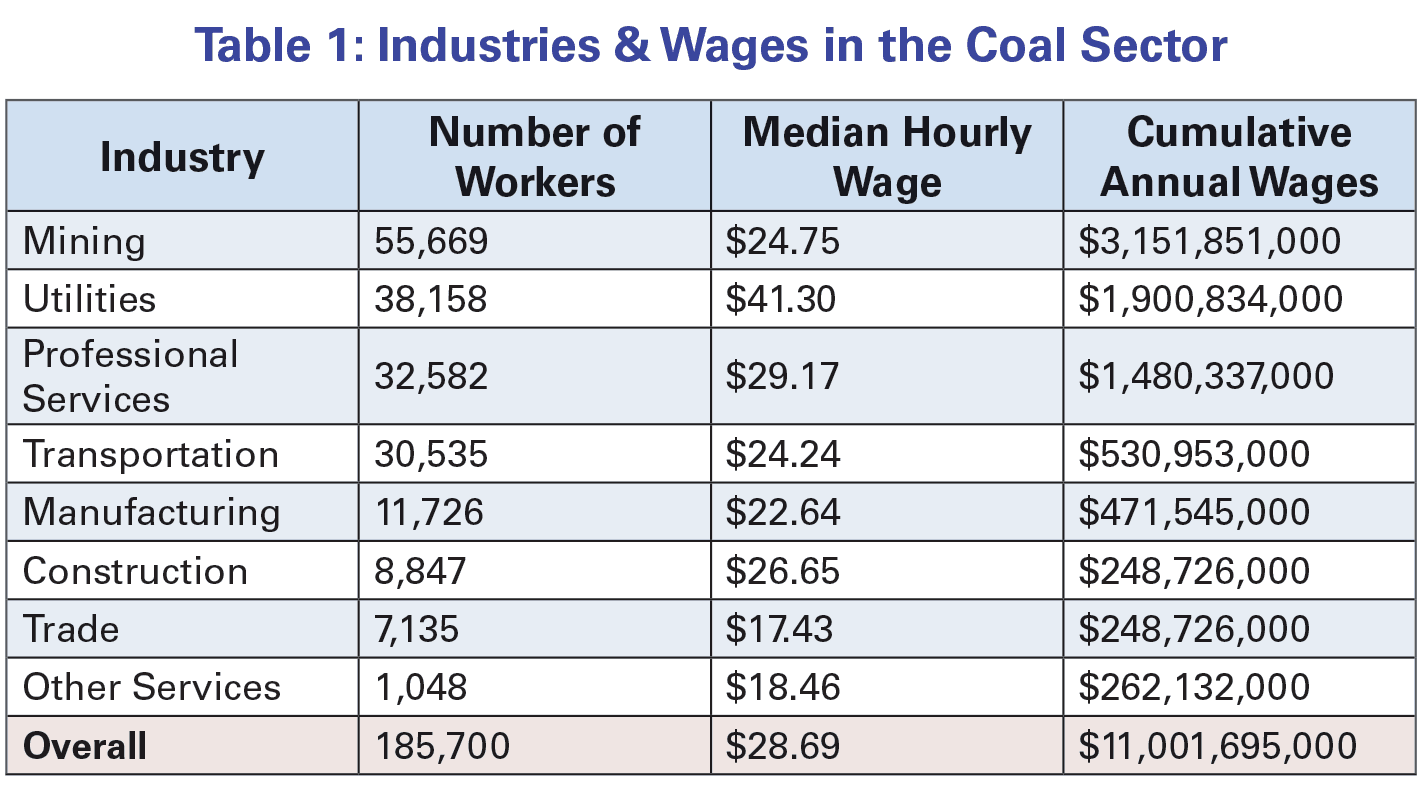

The U.S. coal industry employed about 185,700 people as of 2019, 2.2 percent of total energy employment (see Table above). At $28.69, coal sector jobs on average earn 49.9 percent more than the national median wage and 16 percent more than energy jobs (average energy sector wages are just about $25 an hour – more than a third above the national median). Coal jobs are various, ranging from construction workers for coal plants to those involved in financial, legal and other business-related areas. As with the energy sector overall, wages in the coal sector depend on the industry and one’s level of professional training. Workers in mining (which represents the largest proportion of coal jobs) make less than the coal sector average, while utilities workers (representing the second largest proportion of jobs) earn significantly more.

As policy-makers consider the question of decarbonizing the coal sector, it is important to recognize the skills that its workers possess: deep abilities to learn, well-tested problem-solving skills and the general know-how that is a prerequisite to work in the various industries of this sector. Despite the high wages, coal-related jobs usually do not require advanced degrees. Continuous mining machine operators need no formal education, and power plant operators, electric power-line installers and industrial machinery mechanics require only a high school diploma. But it would be foolhardy to say these jobs are not difficult; most require intensive, long-term on-the-job training and experience, which likely contributes to the higher wages in this industry. While many

of the specific techniques associated with the current coal industries may not be transferrable to new jobs, coal workers have a demonstrated capacity to learn nuanced, complex skills – a valuable ability across industries and occupations.

President Joe Biden has promised to “do right by [coal workers] and make sure they have opportunities to keep building the nation in their own communities and getting paid well for it.” President Biden’s commitment is feasible, and it must be followed up with action that does not leave out any coal-dependent communities. In his first week in office, Biden signed executive order 14008, “Tackling the Climate Crisis at Home and Abroad,” which among other things established an Interagency Working Group on Coal and Power Plant Communities and Economic Revitalization. The Working Group released an initial report in April of this year which, as per the language of the executive order, proposed mechanisms by which to direct existing federal funding streams to communities whose livelihoods rely on the coal industry. This thorough report identified $38 billion in federal grants, loans and assistance programs (most of which is not periodically replenished) from federal departments that coal-dependent communities could access. Coal communities compete with other communities for this funding, but if won, it could fund various coal sector and coal community opportunities from the creation of new small business jobs to the many-year retirement and remediation of coal mines.

This initial Working Group report is a good step in that it identifies a variety of possible development pathways for these communities, including pathways outside the energy sector. The geography of domestic energy is shifting, and replacing coal with offshore wind is not an option for landbound communities in West Virginia or the Mountain West. As policy-makers at national and subnational levels continue increasing their climate ambition, it is imperative that they also provide fair opportunities for the coal industry and its workers along the decarbonization pathway – ideally, by providing funding specifically for the development of new pathways for coal communities in addition to this $38 billion in federal funding. To this end, we present several observations and recommendations which may serve the coal sector and communities well:

- The federal government should assemble information on the skill competencies of jobs within the coal sector to pinpoint opportunities for developing the industry that are congruent with decarbonization. This could provide the opportunity to expand some areas of the coal sector based on industry skillsets (such as developing and implementing carbon capture and storage technology), which could compensate for the stark decrease in coal employment over recent years. The Department of Labor’s O*NET database documents occupation-specific skillsets for a variety of fields, but fine-grained information on the skillsets required for different jobs within each coal industry is lacking. The Department of Energy and the Interagency Working Group could collaborate with individuals across the coal sector to assemble this knowledge.

- Work with state and local government to identify the specific, locally appropriate economic opportunities for coal businesses and their communities. The appropriateness of these opportunities should be based on the skills of the local coal industry workers as identified above, the preferences of the communities and how realistic those options are within the geographic, socioeconomic and cultural context of the area. Re-training coal sector workers to work to improve the energy efficiency of coal production and to develop renewables can be a good choice, but it is not a panacea. A variety of opportunities exist in other sectors, some of which would require retraining and others that would not. Identifying and implementing these opportunities will be crucial both for coal communities affected by the shrinking number of well-paying local jobs and for the coal sector as a whole.

- Federal funding for the coal sector and affiliated communities should reflect the full scale of the coal sector, specifically the costs associated with actualizing economic opportunities for

the sector and maintaining vibrant communities. Much of the information on the size of the coal sector is available in the U.S. Energy & Employment Report. It should be utilized, along with the additional information garnered above (particularly the costs of supporting different avenues of economic development), to identify economic opportunities along the decarbonization pathway that mitigate the continued downsizing of the industry and keep communities healthy. - Consolidate the funding opportunities into an easily accessible, widely publicized “one-stop shop” as proposed in the Working Group’s initial report. This portal should be made directly available to affected coal sector communities and businesses. While references to existing general funding opportunities (i.e., the $38 billion discussed above) would be useful, more useful would be virtually-guaranteed funding opportunities dedicated specifically to affected coal sector communities and to decarbonization-friendly innovation within the coal sector.

Max Dorman is research assistant and Philip Jordan is vice president at BW Research Partnership.